So, you're thinking about buying a house, huh? Let's face it, buying a home is one of the biggest decisions you'll ever make in life. And let me tell you, getting a chase pre approval mortgage is like your golden ticket to making that dream a reality. It’s not just about finding the right house; it's about securing the right financial backing to make it happen. So, buckle up, because we’re diving deep into everything you need to know about chase pre approval mortgages. You won’t regret it, trust me.

Now, you might be wondering, “Why should I care about pre-approval?” Well, here's the deal: a chase pre approval mortgage isn’t just a formality. It’s a powerful tool that gives you an edge in a competitive real estate market. When sellers see that you’ve got pre-approval from Chase, they know you’re serious and financially ready to close the deal. It’s like walking into a car dealership with cash in hand—except this is way bigger.

Let’s not forget the peace of mind that comes with it. Knowing exactly how much house you can afford takes away a lot of the stress and guesswork. So, whether you're a first-time homebuyer or a seasoned pro, understanding the ins and outs of chase pre approval mortgages is crucial. And lucky for you, that’s exactly what we’re going to cover today.

Read also:Tesla Defaced With Swastika Shocks Owner The Incident That Sparked Global Outrage

Here’s a quick roadmap of what’s ahead:

- What is a Chase Pre-Approval Mortgage?

- Why Pre-Approval Matters

- How to Get Pre-Approved with Chase

- Documents You’ll Need

- Common Misconceptions

- Benefits of Pre-Approval

- Chase Mortgage Options

- Tips for a Strong Pre-Approval

- What Happens After Pre-Approval?

- Final Thoughts and Next Steps

What is a Chase Pre-Approval Mortgage?

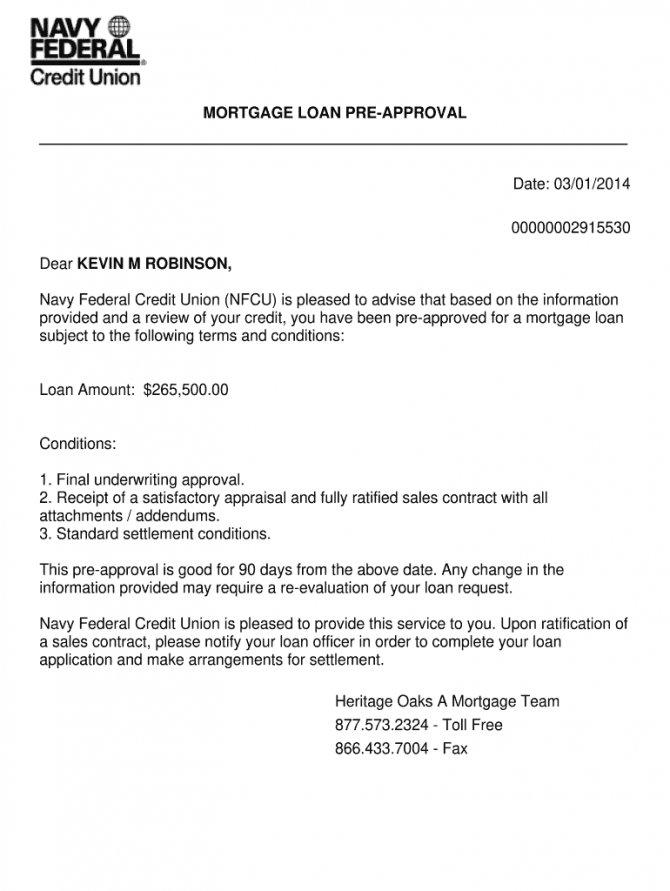

A chase pre approval mortgage is basically a lender’s way of saying, “Hey, we’ve looked at your financials, and we think you’re good to borrow up to this amount.” It’s like a pre-game warm-up before the big game of homeownership. Chase, one of the biggest names in banking, offers this service to help potential buyers get a leg up in the homebuying process.

When you apply for a pre-approval, Chase will take a close look at your credit score, income, debt-to-income ratio, and other financial factors. Based on all that info, they’ll give you a letter stating how much you’re approved to borrow. This isn’t a guarantee, but it’s a strong indication that you’re on the right track.

Think of it as your financial blueprint for buying a home. It tells you exactly how much house you can afford, which neighborhoods you can consider, and gives you confidence when making an offer. And trust me, in today’s market, confidence is key.

Why Choose Chase for Pre-Approval?

Chase is no stranger to the mortgage game. They’ve been helping people buy homes for decades, and they’ve got a reputation for being reliable and customer-focused. Here are a few reasons why Chase stands out:

- Competitive Rates: Chase offers some of the best mortgage rates in the industry.

- Customer Support: Their team is always ready to answer your questions and guide you through the process.

- Convenience: You can apply for pre-approval online, in-person, or over the phone. It’s super flexible.

Why Pre-Approval Matters

Let’s get real for a second. In today’s crazy real estate market, sellers don’t have time for wishy-washy buyers. If you show up without pre-approval, you’re already behind the eight ball. Pre-approval shows sellers that you’re serious and financially ready to close the deal. It’s like showing up to a job interview with your resume already in hand.

Read also:Death Of Former Lincoln Mayor And State Senator Don Wesely A Legacy Worth Remembering

But it’s not just about impressing sellers. Pre-approval also helps you as a buyer. It sets a clear budget, so you’re not wasting time looking at homes you can’t afford. Plus, it gives you leverage when negotiating with sellers. If they know you’re pre-approved, they’re more likely to take your offer seriously.

And let’s not forget the peace of mind factor. Knowing exactly how much house you can afford takes away a lot of the stress and uncertainty. You can focus on finding the perfect home instead of worrying about the finances.

How Pre-Approval Differs from Pre-Qualification

Here’s where things can get a little confusing. Pre-qualification and pre-approval sound similar, but they’re not the same thing. Pre-qualification is like a rough estimate based on your self-reported financial info. It’s quick and easy, but it doesn’t carry as much weight.

Pre-approval, on the other hand, is a much more thorough process. Chase will verify all your financial info, pull your credit report, and give you an official letter stating how much you’re approved to borrow. It’s like the difference between a handshake and a signed contract. Sellers take pre-approval much more seriously.

How to Get Pre-Approved with Chase

Getting pre-approved with Chase is easier than you might think. Here’s a step-by-step guide to help you through the process:

- Gather Your Documents: You’ll need proof of income, bank statements, tax returns, and other financial info.

- Check Your Credit Score: Chase will pull your credit report, so it’s a good idea to know where you stand beforehand.

- Apply Online or In-Person: Chase makes it easy to apply either way. Just fill out the application and wait for their decision.

- Review Your Pre-Approval Letter: Once you’re approved, Chase will send you a letter detailing how much you can borrow.

It’s important to note that pre-approval isn’t a one-size-fits-all process. Chase will tailor their decision based on your unique financial situation. So, don’t stress if you don’t meet all the traditional requirements. They’ve got options for everyone.

Tips for a Strong Pre-Approval Application

Here are a few tips to help you ace your pre-approval application:

- Pay Down Debt: Lowering your debt-to-income ratio can improve your chances of approval.

- Boost Your Credit Score: Even a small increase can make a big difference.

- Be Honest: Don’t exaggerate your financial info. Chase will verify everything, so it’s better to be upfront.

Documents You’ll Need

When applying for a chase pre approval mortgage, you’ll need to provide a few key documents. Here’s a breakdown of what to expect:

- Proof of Income: Pay stubs, W-2 forms, or tax returns.

- Bank Statements: Chase will want to see your account balances and transaction history.

- Credit Report: They’ll pull this themselves, but it’s good to know your score beforehand.

- Asset Information: If you have investments or other assets, be prepared to provide details.

Don’t worry if you don’t have all these documents right away. Chase will guide you through the process and let you know exactly what they need.

Common Misconceptions About Pre-Approval

There are a few myths floating around about pre-approval that I want to clear up:

- Pre-Approval Guarantees a Loan: Nope. It’s just an indication that you’re likely to be approved.

- You Have to Use the Same Lender: Not true. Pre-approval doesn’t lock you into using Chase or any other lender.

- It’s Only for First-Time Buyers: Wrong again. Pre-approval is for anyone looking to buy a home.

Benefits of Pre-Approval

So, why should you bother with pre-approval? Here are a few benefits that make it worth your time:

- Clear Budget: Know exactly how much house you can afford.

- Seller Confidence: Sellers are more likely to take your offer seriously.

- Peace of Mind: Less stress and uncertainty in the homebuying process.

And let’s not forget the competitive edge. In a hot market, having pre-approval can make all the difference. Sellers are more likely to choose an offer from a pre-approved buyer over someone who’s still figuring out their finances.

Chase Mortgage Options

Chase offers a variety of mortgage options to fit different needs. Whether you’re a first-time buyer, a veteran, or someone looking to refinance, they’ve got something for you. Here are a few of their most popular options:

- Conventional Mortgages: For buyers with good credit and a solid down payment.

- FHA Loans: Great for first-time buyers with lower credit scores.

- VA Loans: For veterans and active-duty military personnel.

Tips for a Strong Pre-Approval

Here are a few final tips to help you secure a strong pre-approval:

- Be Prepared: Gather all your documents before applying.

- Work on Your Credit: Even a small improvement can make a big difference.

- Stay Honest: Don’t exaggerate your financial info. Chase will verify everything.

And remember, pre-approval is just the first step. Once you’re approved, it’s time to start house hunting. But don’t rush the process. Take your time to find the perfect home that fits your budget and lifestyle.

What Happens After Pre-Approval?

Once you’re pre-approved, the real fun begins. You’ll start looking at homes, making offers, and negotiating with sellers. Chase will be there every step of the way, guiding you through the process and helping you close the deal. Just remember to stay within your budget and don’t let the excitement get the best of you.

Final Thoughts and Next Steps

So, there you have it. Everything you need to know about chase pre approval mortgages. It’s a powerful tool that can make all the difference in the homebuying process. Whether you’re a first-time buyer or a seasoned pro, pre-approval is a must-have.

Here’s what you should do next:

- Gather your financial documents.

- Check your credit score.

- Apply for pre-approval with Chase.

And don’t forget to share this article with anyone you know who’s thinking about buying a home. The more people understand the importance of pre-approval, the better off we’ll all be. So, what are you waiting for? Go out there and start your homebuying journey. You’ve got this!